Cyprus differs from most other offshore jurisdictions, in that it offers a big number of double tax treaties (44 in total), for the avoidance of double taxation. In general most of the conventions provide reduced rates of withholding taxes on dividends, interest and royalties paid out of the contracting state, or the avoidance of double taxation in the case where a resident in one of the contracting states derives income from the other contracting state. This is one of the key areas which makes Cyprus as an International and Offshore Business Centre unique and respectable.

Cyprus has concluded an impressive number of Double Tax Treaties, something which tax heavens lack in almost all cases. The following treaties are currently in force:

| Armenia | India | Serbia |

| Austria | Ireland | Seychelles |

| Belarus | Italy | Singapore |

| Belgium | Katar | Slovakia |

| Bulgaria | Kirzikstan | Slovenia |

| Canada | Kuwait | South Africa |

| China | Lebanon | Sweden |

| Czech Republic | Malta | Syria |

| Denmark | Mauritius | Tajikistan |

| Egypt | Moldova | Thailand |

| France | Montenegro | Ukraine |

| Romania | Norway | United Kingdom |

| Germany | Poland | USA |

| Greece | Russia | Uzbekistan |

| Hungary | San Marino |

The following table summarizes the withholding tax rates applicable for dividends, interest and royalties paid from the countries shown to residents of Cyprus (for numbers in parenthesis (n) refer to the notes below):

| Country | Paid from countries Shown to residents of Cyprus | ||

| Dividends | Interest | Royalties | |

| Armenia | 0% | 0% | 0% |

| Austria | 10% | 0% | 0% |

| Belarus | 5% (26) | 5% | 5% |

| Belgium | 10% (25) | 10% (4) | 0% |

| Bulgaria | 5% (19) | 7% (1) | 10% |

| Canada | 15% | 15% (1) | 10% (2) |

| China | 10% | 10% | 10% |

| Czech Republic | 0% (20) | 0% | 10% |

| Denmark (30) | 10% (5) | 10% (6) | 0% |

| Egypt | 15% | 15% | 10% |

| France | 10% (7) | 10% (6,10) | 0% (8) |

| Romania | 10% | 10% (4) | 5% |

| Germany | 10% (5) | 10% (4,10) | 0% (8) |

| Greece | 25% (31) | 10% | 0% (11) |

| Hungary | 5% (12) | 10% (4) | 0% |

| India | 10% (7) | 10% (4) | 15% (9) |

| Ireland | 0% | 0% | 0% (11) |

| Italy | 15% | 10% | 0% |

| Katar | 0% | 0% | 5% |

| Kirzikstan | 0% | 0% | 0% |

| Kuwait | 10% | 10% (4) | 5% (3) |

| Lebanon | 5% | 5% (4) | 0% |

| Malta | 0% | 10% (4,10) | 10% (32) |

| Mauritius | 0% | 0% | 0% |

| Moldova | 5% (33) | 5% | 5% |

| Montenegro | 10% | 10% | 10% |

| Norway | 5% (13) | 0% | 0% |

| Poland | 10% | 10% (4) | 5% |

| Russia | 5% (18) | 0% | 0% |

| San Marino | 0% | 0% | 0% |

| Serbia | 10% | 10% | 10% |

| Seychelles | 0% | 0% | 5% |

| Singapore | 0% | 10 (27,4) | 10% |

| Slovakia | 10% (4) | 10% | 5% (3) |

| Slovenia (28) | 10% | 10% | 10% |

| South Africa | 0% | 0% | 0% |

| Sweden | 5% (12) | 10% (4,10) | 0% |

| Syria | 0% (20) | 10% (1) | 15% (21) |

| Tajizikstan | 0% | 0% | 0% |

| Thailand | 10% | 15% (22) | 5% (23) |

| Ukraine | 0% | 0% | 0% |

| United Kingdom | 0% (14) | 10% | 0% (8) |

| USA | 15% (15) | 10% (34) | 0% |

| Uzbekistan | 0% | 0% | 0% |

Notes to the table above:

- Nil if paid to the Government of the other State or for export guarantee

- Nil on literary, dramatic, musical or artistic work

- Nil for literary, artistic or scientific work, film and TV royalties

- Nil if paid to the Government of the other State

- 15% if received by a company holding directly less than 25% of the capital

- Nil if paid to the Government of the other State, or in respect of bank loans, or in connection with the sale on credit of any industrial commercial or scientific equipment or any merchandise

- 15% if received by a company holding directly less than10% of the capital

- 5% on film and TV royalties

- 10% applies to technical service fees. The 10% domestic rate will apply in all other cases as it is lower.

- As a result of changes in local legislation, there is no withholding tax on payments of dividends and interest to foreigners thus the rates provided in the treaty would not apply in practice

- 5% on film royalties

- 15% if received by a company holding directly less than 25% of the capital

- 0% if received by a company holding directly less than 50% of the voting power

- Under the treaty, the rate is 15%, but the domestic rate is 0%

- 5% if received by a company controlling 10% or more of the voting power.

- Nil if paid to the Government of the other State, banks or financial institutions

- 10% on literary artistic or scientific work, film and TV royalties

- 10% if received by a company that has directly invested in the capital of the paying company less than the equivalent of 100.000 US dollars. In the new treaty the amount will be 100.000 Euro.

- 5% if received by a company holding directly of least 25% of the share capital. Otherwise 10%.

- 15% if received by a company holding directly less than 25% of the voting rights.

- 10% on literary, artistic or scientific work including cinematograph films and films of tapes for television or radio broadcasting.

- 10% if paid to financial institution (including an insurance company) or if paid in connection with the sale on credit of any industrial, commercial or scientific equipment, or if paid in connection with the sale on credit of any merchandise by one enterprise to another enterprise.

- The 5% rate applies to copyright royalties paid in respect of literary, dramatic, musical, artistic or scientific work, including software, and film and broadcasting royalties. The 10% rate applies to royalties paid in respect of industrial, commercial and scientific equipment. The rate is 15% for patent and trademark royalties.

- 10% for industrial, commercial or scientific equipment.

- 15% if received by a company holding directly at least 25% of the share capital.

- 5% if received by a company that invested in share capital not less than € 200.000. 10% if paid to a person holding at least 25% of the capital. In all other cases 15%.

- 7% if received by a bank or similar financial institution.

- A new double taxation agreement has been agreed and will have effect when it has been formally ratified by both counties. The new rates will be 5% withholding tax on dividends, interest and royalties.

- 0% if received by a company holding directly less than 10% of the capital. 5% in all other cases.

- New treaty has been signed, but is not yet in effect.

- For 2011, the dividend withholding tax rate is 21%. The rate increases to 25% as from January 2012.

- As a result of changes in local legislation, there is no withholding tax on payments of royalties to foreigners, thus the rates provided by the treaty would not apply in practice.

- This rate applies if received by a company controlling more than 25% of the capital. In all other cases 10% rate applies.

- Interest is exempt if beneficially derived by a resident of a Contracting State with respect to debt obligations guaranteed or insured by that Contracting State (instrumentality), a bank or other financial institution, or a resident with respect to debt obligations arising in connection with the sale of property or the performance of services. Otherwise the rate is 10%.

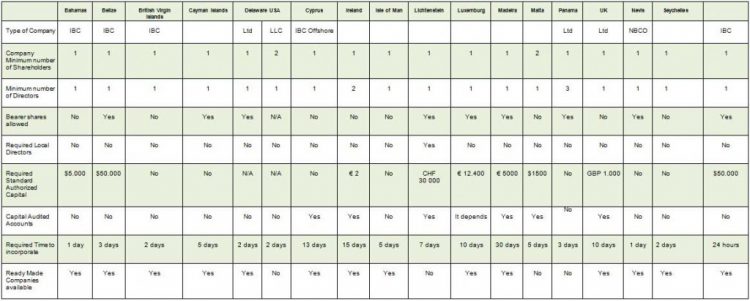

ComparisonChartofDifferentJurisdictions

Please click table to enlarge it.